Grant's Pub annually puts together a free Summer Break and Winter Break issue of the much lauded Grant's Interest Rate Observer. Embedded below is the 2012 Winter Break Issue. Enjoy.

Grant's Interest Rate Observer Winter Break Edition

MONEY IN STEREO

Saturday, December 29, 2012

Thursday, December 20, 2012

Jeff Gundlach on Bloomberg TV

Gundlach has been one of the most successful fixed income managers over the last decade. Gundlach is eclectic and often has an interesting and worthwhile variant view on the markets. In this 20 minute interview, he touches on his bullishness on Japan, his affinity for cash, what he thinks of the Homebuilders, and why he thinks the puny returns on cash will be much appreciated compared to the large losses that could be incurred when the market 're-prices' to the downside.

How to Manually add Playlists from iTunes 11 to your iPhone

"Simplicity is the ultimate sophistication."

-Leonardo Da Vinci

One of the things that has made Apple (AAPL) wildly successful is their ability to create user intuitive products. Steve Jobs said that he first designed the desired user experience, then built a product that would achieve that experience. I think this is one of the most fundamental drivers of AAPL's success and appeal over the years. Now that Jobs is gone, is Apple starting to stray from the path?

iTunes 11 is visually appealing at first glance, but even as an very experienced iTunes user (abuser), I had some trouble getting around. I wanted to drag and drop a playlist from iTunes 11 to my iPhone 4 and run out the door this morning. I sat in front of my Macbook Pro puzzled and confused. I found the answer of how to do it, and for the sake of brevity, I'll withhold any further pontifications in regards to the future of AAPL, and post the answer below.

Hope you find this useful!

-Leonardo Da Vinci

One of the things that has made Apple (AAPL) wildly successful is their ability to create user intuitive products. Steve Jobs said that he first designed the desired user experience, then built a product that would achieve that experience. I think this is one of the most fundamental drivers of AAPL's success and appeal over the years. Now that Jobs is gone, is Apple starting to stray from the path?

iTunes 11 is visually appealing at first glance, but even as an very experienced iTunes user (abuser), I had some trouble getting around. I wanted to drag and drop a playlist from iTunes 11 to my iPhone 4 and run out the door this morning. I sat in front of my Macbook Pro puzzled and confused. I found the answer of how to do it, and for the sake of brevity, I'll withhold any further pontifications in regards to the future of AAPL, and post the answer below.

Hope you find this useful!

How to manually add playlists from iTunes 11 to your iPhone.

1 - Connect your device so that it can be seen in iTunes 11

2 - Select your device and then select "On This iPhone" on the far right (or whatever your connected device is)

3 - Under the blue "Done" button there is another button titled "Add to". Select this

4 - You will now be presented with your iTunes library for your computer. You can select one of the following options for searching your library

5 - Simply drag track(s), albums or playlists over to the iPhone mounted on the right side of iTunes

h/t Robbo

4 - You will now be presented with your iTunes library for your computer. You can select one of the following options for searching your library

h/t Robbo

Wednesday, December 19, 2012

Kyle Bass Keynote: The Engtanglement | AmerCatalyst 2012

In October Kyle Bass gave his keynote presentation, The Entanglement, at the AmerCatalyst 2012 conference. Bass touched on the US, Japan, China and of course the debt related issues. He also spoke a bit about the housing shadow inventory in the Q & A, as well as where he sees some investment opportunities.

Here is the link for the video: Kyle Bass: The Entanglement

h/t Frank Voisin

Here is the link for the video: Kyle Bass: The Entanglement

h/t Frank Voisin

Tuesday, December 4, 2012

It Takes a lot of Work to get to Simple

Einstein said that "everything should be made as simple as possible, but not simpler." It takes a lot of work to get to simple, and the video below shows just that. Here is an interesting perspective of what it takes to make a pencil. It seems simple enough, but how much orchestration occurred to have that simple device conveniently at your finger tips...?

h/t Cook and Bynum

h/t Cook and Bynum

Wednesday, November 28, 2012

Bill Ackman: If You're So Smart, Why Aren't You Rich?

Embedded below is hedge fund activist Bill Ackman's 43 minute presentation that he did a little while back for the Floating University. Initially students or those interested in the video had to pay to see it, but it was just released into public domain on Youtube in it's entirety The title is "Everything You Need to Know About Finance and Investing in Under an Hour." Hmmm...somehow I doubt Ackman covers everything, but he has proven himself to be one of the contemporary greats of the activist/value investment world. Since you'll learn everything you need to know about finance and investing in under an hour, Ackman speaks in broad strokes, but still an educational way to spend some time gleaning insights from a Pro.

A sockless Bruce Berkowtiz interview at University of Miami

Bruce Berkowitz and Fairholme had a rough year in 2011 -to put it mildly- yet has significantly outperformed so far in 2012. During 2011, Berkowitz continued to hold concentrated positions in AIG, Sears, and Bank of American which led him to dramatically trail the market. In 2011, I noticed various talking heads proclaiming the Berkowitz had lost his touch, that he was reckless, and that he was so far under he could not liquidate his positions to meet fund redemptions. Clearly he had lost his touch. Obviously he started taking stupid pills. The pundits were right...wait a minute - no they weren't! Berkowitz remained in his circle of competence, and continued to hold his positions which have produced a 36% return YTD.

Embedded below is a recent interview with Bruce Berkowitz at the University of Miami where he is the "Executive in Residence". He speaks a bit about his General Growth Properties position, his charitable work at the Fairholme Foundation, and his work with the Secret Millionaires Club which creates cartoon webisodes to promote financial literacy for children.

Embedded below is a recent interview with Bruce Berkowitz at the University of Miami where he is the "Executive in Residence". He speaks a bit about his General Growth Properties position, his charitable work at the Fairholme Foundation, and his work with the Secret Millionaires Club which creates cartoon webisodes to promote financial literacy for children.

Tuesday, November 20, 2012

Howard Marks latest memo: A Fresh Start (Hopefully)

Below is the latest memo from the ever insightful Howard Marks at Oaktree Capital.

A Fresh Start (Hopefully)

by Howard Marks

That link goes to the Oaktree site where the PDF can be downloaded or read. All of Marks' past memos are posted on that page as well. Marks is one of the few who imparts pearls of investment wisdom that remain relevant through various market and economic periods. His memos are all there for free, or you can read the cliff notes version in his excellent book: The Most Important Thing: Uncommon Sense for the Thoughtful Investor.

A Fresh Start (Hopefully)

by Howard Marks

That link goes to the Oaktree site where the PDF can be downloaded or read. All of Marks' past memos are posted on that page as well. Marks is one of the few who imparts pearls of investment wisdom that remain relevant through various market and economic periods. His memos are all there for free, or you can read the cliff notes version in his excellent book: The Most Important Thing: Uncommon Sense for the Thoughtful Investor.

GMO's Jeremy Grantham: "On the Road to Zero Growth" Q3 2012 Letter

The latest from Jeremy Grantham of GMO, with additional commentary from Ben Inker.

"On the Road to Zero Growth" - Grantham pgs. 1-17

"Help, Help, I'm Being Repressed" - Inker pgs. 18-20

GMO3Q12 Letter

"On the Road to Zero Growth" - Grantham pgs. 1-17

"Help, Help, I'm Being Repressed" - Inker pgs. 18-20

GMO3Q12 Letter

Sunday, October 28, 2012

Classic Cocktails: The Last Word

The Last Word consists of Gin, Green Chartreuse, Maraschino Liqueur, and Lime Juice all in equal parts. The drink is a nice mix of sweet, sour, and pungent. It's crisp and complex and is deceptively strong, mostly in part to the Green Chartreuse which weighs in with a 55% alcohol content. It's a great cocktail that challenges and refreshes the pallet. Enjoy!

|

| Having the Last Word at the house |

The Last Word

1oz. Gin

1oz. Green Chartreuse

1oz. Maraschino Liqueur

1oz. Fresh squeezed and strained Lime Juice

Here is Robert Hess making the Last Word.

Friday, October 26, 2012

Hugh Hendry and David Einhorn

The video below is a recent one of Hugh Hendry followed by David Einhorn at the Buttonwood gathering in New York City. The topics discussed are the topics that everyone is discussing ad nauseum, eg., Europe's 'Theatre of the Absurd', questions about China's flailing role as the global engine of growth, The US recession and of course the Federal Reserve. If all this has been discussed ad nauseam, then why post a lengthy video of it here?

Two reasons:

1. Hugh Hendry's macro views are well thought out, challenge conventional wisdom, and take into 2nd, 3rd, and 4th level affects. I think he is on par with Ray Dalio as far as one of the few macro opinions worth considering. As Howard Marks has correctly stated, it is impossible to predict these global outcomes. In light of that, it is important to be prepared, and part of doing that is to listen to someone like Hendry as he presents multiple plausible outcomes and the collateral damage associated.

2. Around the 55 minute mark David Einhorn takes the stage (after Hendry, I skipped straight to the Einhorn section, so I can't vouch for what's in between). Einhorn doesn't discuss specific securities, but what he does do is give a thorough rebuttal as to why the Fed's ZIRP is not working and will continue to not work. He feels that by punishing savers, you also punish consumption, which punishes sales, which punishes business growth. He explains in much more detail.

FYI: Unfortunately, the video host (not Me!) is asking for your email to watch the video. It didn't do that last night when I watched it on my phone...

Two reasons:

1. Hugh Hendry's macro views are well thought out, challenge conventional wisdom, and take into 2nd, 3rd, and 4th level affects. I think he is on par with Ray Dalio as far as one of the few macro opinions worth considering. As Howard Marks has correctly stated, it is impossible to predict these global outcomes. In light of that, it is important to be prepared, and part of doing that is to listen to someone like Hendry as he presents multiple plausible outcomes and the collateral damage associated.

2. Around the 55 minute mark David Einhorn takes the stage (after Hendry, I skipped straight to the Einhorn section, so I can't vouch for what's in between). Einhorn doesn't discuss specific securities, but what he does do is give a thorough rebuttal as to why the Fed's ZIRP is not working and will continue to not work. He feels that by punishing savers, you also punish consumption, which punishes sales, which punishes business growth. He explains in much more detail.

FYI: Unfortunately, the video host (not Me!) is asking for your email to watch the video. It didn't do that last night when I watched it on my phone...

Watch live streaming video from theeconomist at livestream.com

Wednesday, October 24, 2012

East Coast Asset Management Q3 Letter - Inventing a Flying Machine

I've thought for some time now that Christopher Begg at East Coast writes one of the more interesting quarterly commentaries. Begg always finds a unique way to tie a seemingly unrelated idea or concept to investing, underscoring Munger's philosophy of taking from all discipline's to form one's lattice work of mental models.

Begg writes about East Coast's investment process and their use of checklists to fully understand how they see an investment and why they believe a margin of safety exists. He also writes about the types of investments that East Coast seeks (Compounders, Transformations, and Work-Outs) and where they look to find their ideas. East Coast prospects among the usual value suspects: spin-offs, post bankruptcy re-orgs, irrational sellers, political and economic clouds.

Embedded below is the letter in full.

East Coast 3Q 2012 Letter_Inventing a Flying Machine

Begg writes about East Coast's investment process and their use of checklists to fully understand how they see an investment and why they believe a margin of safety exists. He also writes about the types of investments that East Coast seeks (Compounders, Transformations, and Work-Outs) and where they look to find their ideas. East Coast prospects among the usual value suspects: spin-offs, post bankruptcy re-orgs, irrational sellers, political and economic clouds.

Embedded below is the letter in full.

East Coast 3Q 2012 Letter_Inventing a Flying Machine

Warren Buffett on CNBC

Warren Buffett discusses a range of topics this morning on CNBC with his favorite reporter, Becky Quick.

Buffett on US Housing Recovery

Buffett: Global Economy Slowing Buffett: Instincts go against QE3 Buffett: We Mostly Buy Stocks for Future Earnings Buffett: We will add 8,000 jobs organically Buffett: We Buy on an all Equity Basis GE's Immelt: Trend is still positive with volatility Where Buffett is Investing Now Buffett: Election comes down to who has a better Ground Game Buffett: Eurozone Banking Problems Cloud Recovery Buffett's Final Word: Hold

Sunday, October 21, 2012

NCAT: Don't fear the FOMO

Much attention has been brought to the area of behavioral economics in the past decade, and rightfully so. To paraphrase Charlie Munger, "If economics isn't behavioral, then what the hell is it?" Benjamin Graham had this to say long before behavioral economics was widely considered as relevant as it is today: “The investor’s chief problem — and even his worst enemy — is likely to be himself.”

Shooting one's self in one's foot while investing frequently happens when an investor's emotions override and suppress clear and logical thought. These emotions span a broad range of fear, euphoria, greed, envy, information overload, uninformed decision making, thumbsucking, confirmation bias, and on and on. (For the definitive guide on emotional bias in decision making see Munger's "The Psychgology of Human Misjudgement" found in Poor Charlie's Almanack.)

In adhering to Munger's advice of taking main ideas from other disciplines and applying them across other mental models, I lifted the NCAT technique from the discipline of clinical psychology. NCAT is an acronym representing a method for handling and addressing internal conflicts, biases, and unruly emotions. Warren Buffett's comments on his Dale Carnegie classes come to mind: “I did not take the course to prevent my knees from shaking when public

speaking . . . but to do public speaking while my knees were knocking.” NCAT reminds me of just that - not crushing or suppressing feelings of anxiety or fear or sadness or uncertainty or anger or disappointment, but rather to competently move forward with the task at hand while those feelings are present.

classes come to mind: “I did not take the course to prevent my knees from shaking when public

speaking . . . but to do public speaking while my knees were knocking.” NCAT reminds me of just that - not crushing or suppressing feelings of anxiety or fear or sadness or uncertainty or anger or disappointment, but rather to competently move forward with the task at hand while those feelings are present.

What does NCAT stand for?

Name it: What are the emotions that I am feeling? It is always best to stop and recognize what is happening internally. By naming the emotion, you bring consciousness to it. With that awareness comes more control over yourself and your actions. Clearly outlining internal motivations is a significant aid in rational decision making.

Claim it: Claim responsibility for those feelings. Often times, anxiety & fear are created in one's own mind. A particular action is only scary because that is how you feel about it. Just because you are afraid of roller coasters or soliciting business from strangers does not mean that these are inherently scary undertakings. They are scary to you because that is the story your mind has built around the experience. By recognizing that our own minds and stories are often responsible for irrational extrapolations of emotion, we can look at a 'scary' situation from a different angle, in a new light, with a different perspective.

Accept it: Accept that you feel the way you do. If it's anxiety that you feel, remind yourself that it is normal to feel anxious at times. "Yes, I feel nervous right now." Everyone feels it whether it shows or not. Stop, take a deep breath and let the anxiety flow through your body and disperse. That harder you try to suppress those feelings, the more concentrated they become, causing more internal tension. By accepting your feelings, you can redirect the energy that it would take to fight how you feel, and channel the energy into more worthwhile endeavors.

Tame it: After going through the previous 3 steps, you should be closer to "taming" what ails you. Move forward and do whatever it is that you originally intended to. By stepping into the unfamiliar, its unfamiliarity ends right then and there. By bringing awareness, responsibility, and acceptance to the unpleasant or unfamiliar you shift your efforts towards achievement rather than defense.

NCAT is something that I use to tone down the emotions inherent when making investment decisions. By using NCAT and seeing a situation with logic, awareness, and consciousness, I can greatly reduce the occurrence of an emotionally charged, short-sighted reaction that I may later regret.

Ex. 1

"This stock has tanked. I am pretty scared at the sight of all that red on my screen. I might have made a poor investment decision. I should just bail."

Ex. 2

"This stock has been a bottle-rocket and I've been sitting on my hands. There are 15 'buy' ratings on it, and I've seen it mentioned about 50 times on a major business news channel. I don't want to be the only one missing out.

In both examples, naming the feelings (anxiety or fear of missing out) brings consciousness and awareness to those emotions. Are those good influencers of decision making? No! Claim those emotions and recognize what is happening inside. Accept that you do feel a strong internal sense of urgency to act on those feelings, even if it is not in your best interest. Tame those emotions by recognizing them, and realizing that the investments should be reexamined and based on fundamental merit rather than the unconscious compulsion to act swiftly and alleviate the near term pain.

Slowing down the process leads to better self examination.

Ex. 1 Revisited

"If I sell this stock, is it because the price is way down and I can't take the pain, or has the story fundamentally changed and permanently impaired the company's future earnings power?"

Ex. 2 Revisited

"If I'm chasing the price upwards, will I still have an adequate margin of safety - even at higher prices? If everyone is already bullish on this stock and expectations are extremely high, what advantage do I have?"

Name It.

Claim It.

Accept It.

Tame It.

{kind=link}

Shooting one's self in one's foot while investing frequently happens when an investor's emotions override and suppress clear and logical thought. These emotions span a broad range of fear, euphoria, greed, envy, information overload, uninformed decision making, thumbsucking, confirmation bias, and on and on. (For the definitive guide on emotional bias in decision making see Munger's "The Psychgology of Human Misjudgement" found in Poor Charlie's Almanack.)

In adhering to Munger's advice of taking main ideas from other disciplines and applying them across other mental models, I lifted the NCAT technique from the discipline of clinical psychology. NCAT is an acronym representing a method for handling and addressing internal conflicts, biases, and unruly emotions. Warren Buffett's comments on his Dale Carnegie

What does NCAT stand for?

Name it: What are the emotions that I am feeling? It is always best to stop and recognize what is happening internally. By naming the emotion, you bring consciousness to it. With that awareness comes more control over yourself and your actions. Clearly outlining internal motivations is a significant aid in rational decision making.

Claim it: Claim responsibility for those feelings. Often times, anxiety & fear are created in one's own mind. A particular action is only scary because that is how you feel about it. Just because you are afraid of roller coasters or soliciting business from strangers does not mean that these are inherently scary undertakings. They are scary to you because that is the story your mind has built around the experience. By recognizing that our own minds and stories are often responsible for irrational extrapolations of emotion, we can look at a 'scary' situation from a different angle, in a new light, with a different perspective.

Accept it: Accept that you feel the way you do. If it's anxiety that you feel, remind yourself that it is normal to feel anxious at times. "Yes, I feel nervous right now." Everyone feels it whether it shows or not. Stop, take a deep breath and let the anxiety flow through your body and disperse. That harder you try to suppress those feelings, the more concentrated they become, causing more internal tension. By accepting your feelings, you can redirect the energy that it would take to fight how you feel, and channel the energy into more worthwhile endeavors.

Tame it: After going through the previous 3 steps, you should be closer to "taming" what ails you. Move forward and do whatever it is that you originally intended to. By stepping into the unfamiliar, its unfamiliarity ends right then and there. By bringing awareness, responsibility, and acceptance to the unpleasant or unfamiliar you shift your efforts towards achievement rather than defense.

NCAT is something that I use to tone down the emotions inherent when making investment decisions. By using NCAT and seeing a situation with logic, awareness, and consciousness, I can greatly reduce the occurrence of an emotionally charged, short-sighted reaction that I may later regret.

Ex. 1

|

The Hot Seat |

Ex. 2

"This stock has been a bottle-rocket and I've been sitting on my hands. There are 15 'buy' ratings on it, and I've seen it mentioned about 50 times on a major business news channel. I don't want to be the only one missing out.

In both examples, naming the feelings (anxiety or fear of missing out) brings consciousness and awareness to those emotions. Are those good influencers of decision making? No! Claim those emotions and recognize what is happening inside. Accept that you do feel a strong internal sense of urgency to act on those feelings, even if it is not in your best interest. Tame those emotions by recognizing them, and realizing that the investments should be reexamined and based on fundamental merit rather than the unconscious compulsion to act swiftly and alleviate the near term pain.

Slowing down the process leads to better self examination.

Ex. 1 Revisited

"If I sell this stock, is it because the price is way down and I can't take the pain, or has the story fundamentally changed and permanently impaired the company's future earnings power?"

Ex. 2 Revisited

"If I'm chasing the price upwards, will I still have an adequate margin of safety - even at higher prices? If everyone is already bullish on this stock and expectations are extremely high, what advantage do I have?"

Name It.

Claim It.

Accept It.

Tame It.

Friday, October 19, 2012

Wednesday, October 17, 2012

See where the Internet lives

Charlie Munger was quoted at a Berkshire shareholder meeting a couple of years back saying that he thought Google had one of the widest economic moats he had ever encountered after reading In The Plex.

This inside look at their data centers is visual support to that claim. I also remember in the Columbia Business School Class presentations Glenn Greenberg citing Google's tremendous infrastructure and world class talent pool/attraction as competitive advantages. All investment pontifications aside, a look under the hood at Google is quite impressive!

Check out this Wired.com story on the data centers as well as Google's own photo gallery linked just below.

Where the Internet Lives: Google Data Center Photo Gallery

.PNG)

.PNG)

.PNG)

.PNG)

This inside look at their data centers is visual support to that claim. I also remember in the Columbia Business School Class presentations Glenn Greenberg citing Google's tremendous infrastructure and world class talent pool/attraction as competitive advantages. All investment pontifications aside, a look under the hood at Google is quite impressive!

Check out this Wired.com story on the data centers as well as Google's own photo gallery linked just below.

Where the Internet Lives: Google Data Center Photo Gallery

.PNG)

.PNG)

.PNG)

.PNG)

Charlie Munger Talk at Harvard-Westlake from 2010

Charlie Munger is no doubt one of the greatest minds of today. Not only an investor, but also a philosopher who I believe can be most likened to his role model, The Autobiography of Benjamin Franklin.

Munger's lessons in both life and investing are profoundly insightful. As Charlie often says, it is much better to learn vicariously by studying the folly and triumphs of others, then emulating the appropriate behavior. With that being said, another Mungerism comes to mind that I often remind myself of: A lot of folks ask for advice, but very few take it.

Munger Talk at Harvard-Westlake

Munger's lessons in both life and investing are profoundly insightful. As Charlie often says, it is much better to learn vicariously by studying the folly and triumphs of others, then emulating the appropriate behavior. With that being said, another Mungerism comes to mind that I often remind myself of: A lot of folks ask for advice, but very few take it.

Munger Talk at Harvard-Westlake

Friday, October 12, 2012

Tuesday, October 9, 2012

Steven Romick of FPA interview via GuruFocus

GuruFocus interviewed FPA's Steven Romick one day after QE3 was announced. Here are some of Romick's thoughts on dealing with the macro in the context of being a bottoms up stock picker. He also talks about idea generation and going to where the most negativity is to search for bargains.

Excerpts

GuruFocus: Okay. So talk about the macro picture. What is the macro risk now?

Romick: I think today, the biggest thing is that the central banks think the only way out of this is just to print money, and so we’re in uncharted territory. We’ve taken what was an academic discussion and decided to experiment in the real world. There’s a whole range of outcomes, some that we can identify and others that I’m certain that we can’t identify, and it’s scary. Will we have inflation or deflation? If it is inflation, will it be a deflationary path to inflation? And then, how do we position a portfolio if we don’t have a strong conviction that it’s one or the other, inflation or deflation? What benefits a portfolio in an inflationary world is very different than what benefits a portfolio in a deflationary world. It’s very, very complicated.

On whether HPQ was a mistake:

Romick: It’s to be determined.

Steve Romick GuruFocus interview

Excerpts

GuruFocus: Okay. So talk about the macro picture. What is the macro risk now?

Romick: I think today, the biggest thing is that the central banks think the only way out of this is just to print money, and so we’re in uncharted territory. We’ve taken what was an academic discussion and decided to experiment in the real world. There’s a whole range of outcomes, some that we can identify and others that I’m certain that we can’t identify, and it’s scary. Will we have inflation or deflation? If it is inflation, will it be a deflationary path to inflation? And then, how do we position a portfolio if we don’t have a strong conviction that it’s one or the other, inflation or deflation? What benefits a portfolio in an inflationary world is very different than what benefits a portfolio in a deflationary world. It’s very, very complicated.

On whether HPQ was a mistake:

Romick: It’s to be determined.

Steve Romick GuruFocus interview

Voter Registration Cutoff Today for 17 states!

Today is cutoff day for voter registration for 17 states:

Arizona

Arkansas

Colorado

D.C.

Florida

Georgia

Illinois

Indiana

Kentucky

Louisiana

Michigan

Montana

New Mexico

Ohio

Pennsylvania

Texas

Utah

Rock the Vote Voter Registration link

TERRITORIAL GROWTH OF THE USA

Link to Wikipedia article on US Territorial Acquisitions

Arizona

Arkansas

Colorado

D.C.

Florida

Georgia

Illinois

Indiana

Kentucky

Louisiana

Michigan

Montana

New Mexico

Ohio

Pennsylvania

Texas

Utah

Rock the Vote Voter Registration link

TERRITORIAL GROWTH OF THE USA

|

| As of August 7th, 1789 |

|

| As of October 1st, 1804 |

| |||

| As of March 30th, 1822 |

|

| As of March 2nd, 1853 |

|

| Present day U.S. |

Link to Wikipedia article on US Territorial Acquisitions

Monday, October 8, 2012

Cook & Bynum: A young fund doing all the right things

Embedded below is a recent interview by The Manual of Ideas with Richard Cook and Dowe Bynum of the Cook & Bynum Fund (COBYX). The young managers both have prestigious prior experience working at Goldman Sachs and Tudor Investment Corp, respectively. After reading the interview, I would not let age belie the duo's investment insight and process. There are several traits exhibited in the interview that piqued my interest. Listed are some of the guiding tenants of the Cook & Bynum fund:

1. Astute subscribers to Munger's theory of Metal Models and building a mental latticework on which to hang one's ideas.

2. Buffett & Munger's belief in portfolio concentration - concentrating one's assets in one's best ideas.

3. Buffett & Munger's adherence to only working with the highest quality management with properly aligned incentives.

4. Prefer to buy a great business at a fair price rather than a fair business at a great price.

5. Eating their own cooking. The majority of their net worth is personally invested in the fund.

6. Ben Graham's landmark principle of investing with a Margin of Safety.![]()

The interview below goes into more detail about their background, philosophy, and process. I was a bit disappointed to see a 1.88% expense ratio, but hopefully that will go down as assets under management grow. If Cook & Bynum stick to their guns as outlined in the interview, I would expected a very enviable long term track record.

Manual of Ideas Interview With Cook Bynum With Disclaimers

Disclosure: this is not a recommendation to buy or sell any securities mentioned in this article or anywhere on this website.

1. Astute subscribers to Munger's theory of Metal Models and building a mental latticework on which to hang one's ideas.

2. Buffett & Munger's belief in portfolio concentration - concentrating one's assets in one's best ideas.

3. Buffett & Munger's adherence to only working with the highest quality management with properly aligned incentives.

4. Prefer to buy a great business at a fair price rather than a fair business at a great price.

5. Eating their own cooking. The majority of their net worth is personally invested in the fund.

6. Ben Graham's landmark principle of investing with a Margin of Safety.

The interview below goes into more detail about their background, philosophy, and process. I was a bit disappointed to see a 1.88% expense ratio, but hopefully that will go down as assets under management grow. If Cook & Bynum stick to their guns as outlined in the interview, I would expected a very enviable long term track record.

Manual of Ideas Interview With Cook Bynum With Disclaimers

Disclosure: this is not a recommendation to buy or sell any securities mentioned in this article or anywhere on this website.

Graham and Doddsville Fall Newsletter 2012

The Fall edition of the Graham & Doddsville newsletter from Columbia Business School was released today. The G&D letter is always a great read and this issue is no exception. In this issue there are interviews with Joel Greenblatt, Jim Tisch, Royce Associates, as well as photos from the Graham, Buffett and Beyond dinner in Omaha with speakers Thomas Russo, David Winters and Mario Gabelli.

Graham & Doddsville - Issue 16 - Fall 2012_vFINAL2

Graham & Doddsville - Issue 16 - Fall 2012_vFINAL2

Wednesday, October 3, 2012

Daniel Loeb Third Point Q3 Investor Letter

Embedded below is Daniel Loeb of Third Point's most recent letter to investors. Loeb is one of the few who has continually outperformed the market through a value and activist approach, as well as shifting funds into credit markets when the risk is worth the reward. Loeb shares his thoughts Third Point's foray in the EU debt markets, as well as giving some color on recent equity investments in Murphy Oil and AIG.

On AIG:

"...Treasury’s ultimate sale of its remaining 16% stake in AIG will serve as a critical catalyst for the company, allowing initiation of a dividend, a change in management’s compensation structure to a more standard incentive-based bonus payout model, and the removal of the overhang” of Treasury ownership. Given these multiple paths to value creation, we believe AIG’s current valuation at ~10x consensus 2013 earnings and 0.5x pro forma tangible book value of $65 per share has significant upside from these levels."

Loeb also manages to leave investors with a few choice quotes from 2Pac and Boyz II Men to shed further insights on Third Point's logic.

Third Point Q3 2012 Investor Letter TPOI

On AIG:

"...Treasury’s ultimate sale of its remaining 16% stake in AIG will serve as a critical catalyst for the company, allowing initiation of a dividend, a change in management’s compensation structure to a more standard incentive-based bonus payout model, and the removal of the overhang” of Treasury ownership. Given these multiple paths to value creation, we believe AIG’s current valuation at ~10x consensus 2013 earnings and 0.5x pro forma tangible book value of $65 per share has significant upside from these levels."

Loeb also manages to leave investors with a few choice quotes from 2Pac and Boyz II Men to shed further insights on Third Point's logic.

Third Point Q3 2012 Investor Letter TPOI

Tuesday, October 2, 2012

Zell: "Unreality and why everything is mispriced"

Sam Zell, a self-made real estate titan, is here speaking with the crew on CNBC. Fortunately, they actually let him talk without bulldozing him with agenda based questions. Zell truly has a 20,000ft view of the economy, and he always speaks his mind. His prognosis is not the rosiest.

"We need leadership, not criticism. We need encouragement, not discouragement..."

- Sam Zell

SAM ZELL CNBC INTERVIEW

"We need leadership, not criticism. We need encouragement, not discouragement..."

- Sam Zell

SAM ZELL CNBC INTERVIEW

The Fraud Files

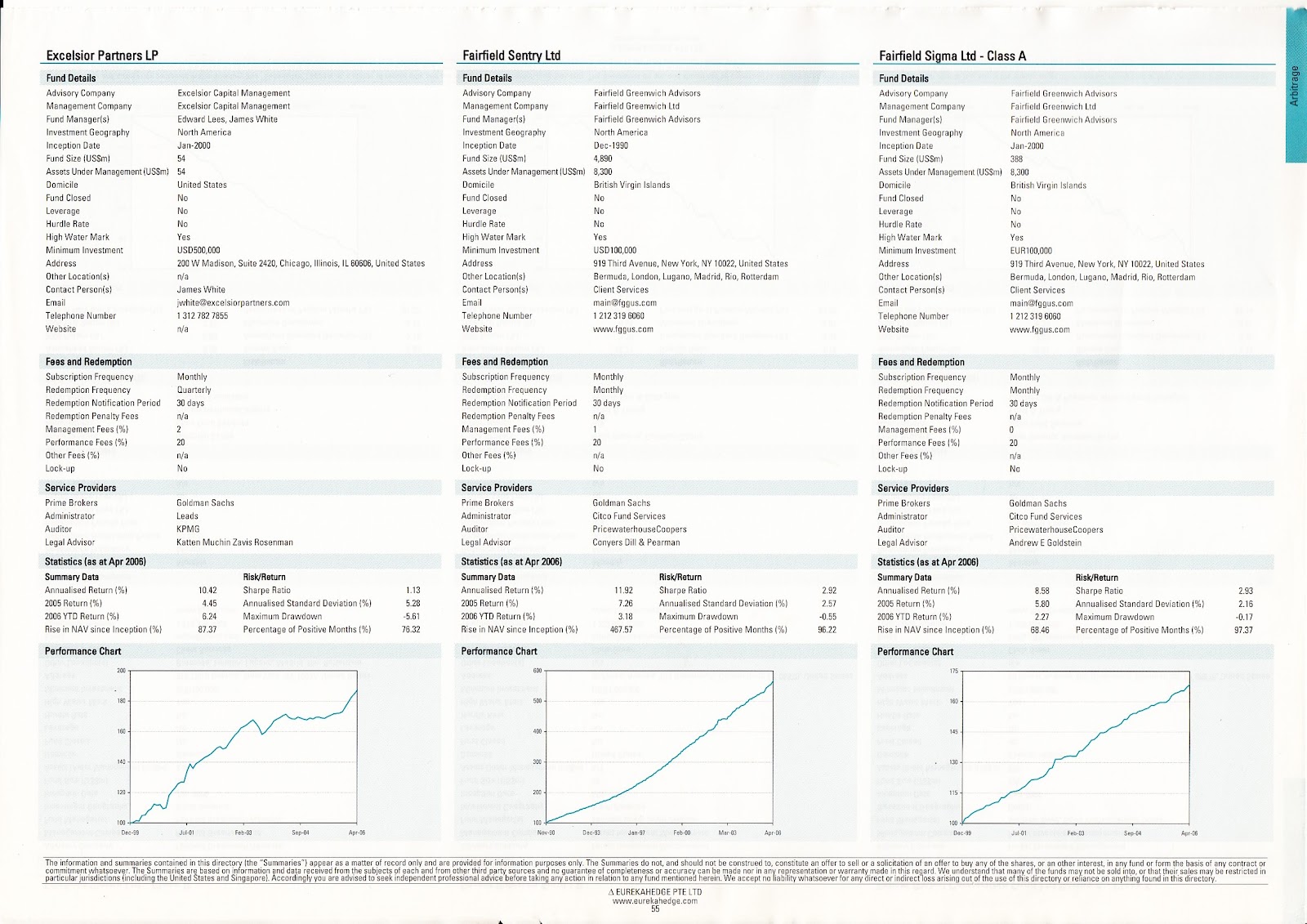

An interesting and quick read found via Santangel's Review showing the chart of one of the Madoff feeder funds. Of course hindsight is 20/20, but looking at the chart of the Fairfield Sentry Fund is truly amazing...if it were real. Cliche I know, but typically if things are too good to be true, then they are. As Charlie Munger says, "There is no way to get rich with soft white hands." Another quote that comes to mind is that of Richard Feynman which says, "The first principle is that you must not fool yourself - and you are the easiest person to fool." I would imagine after being conditioned for decades of steadily upward performance, that one could start to believe in the viability of such "remarkable" performance.

Sentry Fund Fraud Chart

Sentry Fund Fraud Chart

Not so New

Keith Trauner and Larry Pitkowsky are the founders of the Goodhaven Fund (GOODX). The fund is relatively new, but Trauner and Pitkowsky are not, having been integral parts of the team at Fairholme (FAIRX) with Bruce Berkowitz thru his finest years of out performance. The interview linked below talks about their time at Fariholme, their philosophy and understanding of value investing, and the low down on some of their current favorite ideas.

The fund has put up decent numbers in its short existence, beating the S&P this year, though lagging a bit since inception in 2011. Typically value will lag in a rising market as we have seen recently, but that is not all bad. It is a sign that the managers have a clear cut value investment process that they are sticking to. The true test will be in a significant market draw down. If the GOODX managers truly invest with a Ben Graham-like margin of safety, then the fund's downside should be mitigated. Furthermore, the managers have a significant portion of their personal wealth invested in the fund, so you can be assured that portfolio decisions are being made with shareholders best interest in mind.

GOODHAVEN INTERVIEW

disclosure: this is not a recommendation to purchase any securities mentioned in this post or anywhere on the blog. This blog strictly expresses the opinions of the author.

The fund has put up decent numbers in its short existence, beating the S&P this year, though lagging a bit since inception in 2011. Typically value will lag in a rising market as we have seen recently, but that is not all bad. It is a sign that the managers have a clear cut value investment process that they are sticking to. The true test will be in a significant market draw down. If the GOODX managers truly invest with a Ben Graham-like margin of safety, then the fund's downside should be mitigated. Furthermore, the managers have a significant portion of their personal wealth invested in the fund, so you can be assured that portfolio decisions are being made with shareholders best interest in mind.

GOODHAVEN INTERVIEW

disclosure: this is not a recommendation to purchase any securities mentioned in this post or anywhere on the blog. This blog strictly expresses the opinions of the author.

Monday, October 1, 2012

Music page update

FYI - I added a few songs to the TUNES tab in the Amazon player. I ran across Anders Osborne, Junior Brown, Michael Kiwanuka, and another Bass Drum of Death track I thought I should share. The drummer from BDOD is leaving for undisclosed reasons. That's a bummer because he was a real bruiser when we saw them live at One Eyed Jack's in New Orleans. Not sure how that will affect things going forward, but BDOD did say that a new LP was hitting the shelves soon. Looking forward to that!

Recent commentary from FPA's Bob Rodriguez - "All In!"

"It is all about not underperforming the market or a benchmark, so don’t fight the Fed. Unfortunately, a strategy of following the Fed’s urging to take on greater risk will likely end in heartbreak. Should the stock market continue its upward march, both our clients and FPA’s portfolio managers will be tested. This is a time for discipline. Given that economic growth is languid at best and is likely slowing, the divergence between the stock market and economic reality cannot be sustained. One or the other has to adjust."

- Bob Rodriguez

Embedded below is Bob Rodriguez's latest commentary about the Fed's recent QE Infinity announcement. That was a couple weeks ago, and the market's optimism about the maneuver is already fading.

all-in-commentary-9-2012BC714505E176

- Bob Rodriguez

Embedded below is Bob Rodriguez's latest commentary about the Fed's recent QE Infinity announcement. That was a couple weeks ago, and the market's optimism about the maneuver is already fading.

all-in-commentary-9-2012BC714505E176

Saturday, September 29, 2012

Pain is sending a message.

I found the excerpt below via the always insightful Farnam Street Blog.

“When we encounter pain, we are at an important juncture in our decision-making process.”

It is a fundamental law of nature that to evolve one has to push one’s limits, which is painful, in order to gain strength—whether it’s in the form of lifting weights, facing problems head-on, or in any other way. Nature gave us pain as a messaging device to tell us that we are approaching, or that we have exceeded, our limits in some way. At the same time, nature made the process of getting stronger require us to push our limits. Gaining strength is the adaptation process of the body and the mind to encountering one’s limits, which is painful. In other words, both pain and strength typically result from encountering one’s barriers. When we encounter pain, we are at an important juncture in our decision-making process.

Most people react to pain badly. They have “fight or flight” reactions to it: they either strike out at whatever brought them the pain or they try to run away from it. As a result, they don’t learn to find ways around their barriers, so they encounter them over and over again and make little or no progress toward what they want.— Ray Dalio

Friday, July 20, 2012

Ray Dalio - Bridgewater 2012 Q2 Letter to Investors

Ray Dalio, one of the few macro mavens worth listening to, recently came out with his 2012 Q2 letter to investors.

On an interconnected global economy:

"The breadth of this slowdown creates a dangerous dynamic because, given the inter-connectedness of economies and capital flows, one country's decline tends to reinforce another's, making a self-reinforcing global decline more likely and a reversal more difficult to produce."

If China is truly slowing down it's important to think about how this affects the price of commodities and similar inputs to the Chinese economy. How will that affect export countries of those goods?

On Stocks:

On an interconnected global economy:

"The breadth of this slowdown creates a dangerous dynamic because, given the inter-connectedness of economies and capital flows, one country's decline tends to reinforce another's, making a self-reinforcing global decline more likely and a reversal more difficult to produce."

If China is truly slowing down it's important to think about how this affects the price of commodities and similar inputs to the Chinese economy. How will that affect export countries of those goods?

On Stocks:

Wednesday, June 20, 2012

Howard Marks Oaktree Capital: It's all a Big Mistake

Howard Marks' latest memo: "It's all a Big Mistake" is an excellent read on the psychology of investor sentiment, the tendency to overshoot, or to improperly incorporate information into investment decisions. Marks expands on a few points as to why investors tend to not buy assets that are cheap - or at least not enough of them:

is an excellent read that channels a clairvoyance nearly on par with Mr. Buffett.

"Active Management has to be seen as the search for mistakes."

-Howard Marks

FYI - I added a couple books to the "Worthwhile Investment Reading" page:

- Bias or Close-mindedness

- Capital Rigidity

- Psychological Excesses

- Herd behavior

"Active Management has to be seen as the search for mistakes."

-Howard Marks

FYI - I added a couple books to the "Worthwhile Investment Reading" page:

- The Most Important Thing: Uncommon Sense for the Thoughtful Investor (Columbia Business School Publishing)

- There's Always Something to Do: The Peter Cundill Investment Approach

- Competition Demystified: A Radically Simplified Approach to Business Strategy

- Value Investing: From Graham to Buffett and Beyond (Wiley Finance)

How to change a habit.

How to change a habit? Good question. The above diagram depicts the brain's internal process for habit formation and execution. As with many of our reactions, this chain effect is largely on auto pilot. External cues or triggers come to us unexpectedly throughout the day causing these habits or auto-responses in our brains. Obviously not all habits are good, and not all habits are bad. The above diagram can be used as a tool to change those bad habits into good ones.

For more reading about the formation of habits check out The Power of Habit: Why We Do What We Do in Life and Business

"The chains of habit are too light to be felt until they are too heavy to be broken."

-Warren Buffett

Monday, June 18, 2012

Money, Power, & Public Broadcasting

Money, Power, & Wall St. is a new Frontline mini-series that takes a boots on the ground view of Wall Street. Episode 1 goes back to the mid-1990's and traces the origins of the creation of CDO's. That may not sound very interesting at a glance, but when you consider the magnitude and impact that that one synthetic credit 'product' has had on millions of Americans, it should peak one's interest. It was the trade heard round the world. It was a private market that avoided regulation, and "shifted risk" from the banks to the counter party.

Hindsight is 20/20, but amazingly, Greenspan sided with the banks on these opaque derivative markets. It just goes to show that sometimes the smartest minds in the world are blinded by their own self-confidence, the subtle undertow of the crowd, and an inadequate understanding of what they themselves do not know.

I have only watched the first episode, but it seems like a very promising documentary. Frankly, I am very tired of 'blaming' the banks, banksters, hedge funds, private equity, and whomever else we can throw in to the pot. The damage is done. Now we need to fix it. In my viewing of EPS 1, it has been explained the how and the why of the CDS's creation, and hopefully the documentary continues its enlightening look behinds the scenes.

As noted above, this has and continues to affect millions of Americans everyday, therefore, I think it important to understand the beginnings and the evolution of our miseries so as to avoid them in the generations to come.

"Those who cannot remember the past are condemned to repeat it."

-George Santayana

Hindsight is 20/20, but amazingly, Greenspan sided with the banks on these opaque derivative markets. It just goes to show that sometimes the smartest minds in the world are blinded by their own self-confidence, the subtle undertow of the crowd, and an inadequate understanding of what they themselves do not know.

I have only watched the first episode, but it seems like a very promising documentary. Frankly, I am very tired of 'blaming' the banks, banksters, hedge funds, private equity, and whomever else we can throw in to the pot. The damage is done. Now we need to fix it. In my viewing of EPS 1, it has been explained the how and the why of the CDS's creation, and hopefully the documentary continues its enlightening look behinds the scenes.

As noted above, this has and continues to affect millions of Americans everyday, therefore, I think it important to understand the beginnings and the evolution of our miseries so as to avoid them in the generations to come.

"Those who cannot remember the past are condemned to repeat it."

-George Santayana

Watch Money, Power and Wall Street: Part One on PBS. See more from FRONTLINE.

Saturday, June 16, 2012

PBS Wealthtrack - Richard Bernstein and Bill Wilby

Good episode this week with Richard Bernstein and Bill Wilby. Wilby was Oppenheimer Global Portfolio manager for 10 years, which was the #1 ranked fund in its category for the duration of his tenure. Bernstein made his name as Merill Lynch's chief investment strategist. He was ranked in the top investment strategists by his peers for 18 years, 10 of which, he was ranked #1.

Wealthtrack is a weekly show on PBS, and for some reason, they consistently get some of the best investing minds around to interview. They did reruns the previous two weeks, but hopefully they were busy taping new shows and needed some filler.

Wealthtrack is a weekly show on PBS, and for some reason, they consistently get some of the best investing minds around to interview. They did reruns the previous two weeks, but hopefully they were busy taping new shows and needed some filler.

Friday, June 15, 2012

Don't Eat Fortune's Cookie

Michael Lewis, best selling author of Liars Poker and Moneyball, examines the role of luck in people's lives, including his own at the beginning of his career. He urges the fortunate to acknowledge it, and embrace humility.

Thursday, June 14, 2012

The Sazerac, take one

.JPG)

My first attempt at making a Sazerac. Building the home bar one drink at a time.

Check this famous New Orleans bartender out for step by step instructions on how to make this classic cocktail.

Stop Breakin' Down

As mentioned, this blog is about music as well. For those about to rock, I present the "Stop Breakin' Down", a Thirdman Records Vault track from the White Stripes last show ever. This was issued on vinyl only, and only as many copies were printed as there were members of the Thirdman Vault subscription service.

The interesting investment component is that based on law of supply and demand, these records are in limited supply. That's a fact. Thirdman guarantees to never print these again (which would be the same as diluting stock holders thru an equity raise). The market (eBay) has rewarded the quality and scarcity of this record by putting an average auction sale price north of $200 for this "Live in Mississippi" album.

The interesting investment component is that based on law of supply and demand, these records are in limited supply. That's a fact. Thirdman guarantees to never print these again (which would be the same as diluting stock holders thru an equity raise). The market (eBay) has rewarded the quality and scarcity of this record by putting an average auction sale price north of $200 for this "Live in Mississippi" album.

A book and a Berkshire website hack

(1).JPG)

I just got this bad boy today. I'm talking about the book, not the Vox amp. The author Peter Bevelin also wrote the excellent "Seeking Wisdom", so I have pretty high hopes for this book. "A Few Lessons for Investors and Managers" is a condensed easy-to-read essay version spanning all of Buffett's Berkshire Hathaway annual letters as well ask BRK's "Owners Manual".

I would have posted a link to the Owners Manual PDF, but it appears that Berkshire's website has been hacked.

The Vox is about 10 years old. It is solid state with a pretty decent tremelo section built in. I've always been a tube purist, but a while back for fun, I put my D*A*M Red Rooster

in front of it. I had it pushing a mid 1960's 2x12 Fender Bandmaster cabinet. Clearly this 15 watt 8-inch solid state combo is not designed for that, but man! - that Red Rooster lit up the transistors in the Vox. Tons o' fuzzy distortion, plenty of volume. A good time was had by all.

Both books mentioned can be purchased here:

http://www.poorcharliesalmanack.com/

or here thru Amazon:

Subscribe to:

Posts (Atom)